When it comes to Medicaid planning, securing your assets is paramount. A Medicaid Asset Protection Trust (MAPT) offers a strategic solution for protecting your wealth from nursing home expenses and estate recovery programs.

As estate planning attorneys with decades of combined experience, we've helped countless clients implement MAPTs to preserve their legacy while securing access to Medicaid services. This guide provides comprehensive information about how these irrevocable trusts work, their costs, benefits, and limitations to help you make informed decisions about your estate plan.

* Disclaimer: This guide provides general information about Medicaid Asset Protection Trusts and is not intended as legal advice. Medicaid rules and estate planning strategies can be complex and vary by state. We recommend consulting with our experienced attorneys to discuss your specific situation.

What Is a Medicaid Asset Protection Trust (MAPT)?

A Medicaid Asset Protection Trust (MAPT) is an irrevocable trust designed to help individuals qualify for Medicaid benefits while protecting their assets from being counted toward the program's asset limit. By transferring assets into this trust, they're removed from your individual assets for Medicaid eligibility purposes, allowing you to meet the strict financial requirements imposed by the Medicaid program. These trusts serve as a bridge between protecting your wealth and accessing essential long-term care services when needed.

How Does a MAPT Work?

A MAPT functions by transferring ownership of your assets to an irrevocable trust, making them no longer countable toward Medicaid's asset limit. The trust must be established at least five years before applying for Medicaid benefits to avoid penalties during the look-back period. Neither the grantor nor their spouse can serve as trustee, ensuring the assets are truly beyond the applicant's control for Medicaid purposes.

Important note: The five-year look-back period is critical — any assets transferred within this timeframe may result in Medicaid ineligibility penalties.

Planning for a MAPT well in advance is essential, as the trustmaker must establish it at least five years before submitting their Medicaid application to avoid violating the program’s Look-Back Period regulations. This kind of strategic planning ensures that the MAPT fulfills its intended purpose without jeopardizing long-term care planning efforts.

What Are the Benefits of a MAPT?

Setting up a Medicare Asset Protection Trust can confer several notable benefits, including the following.

- Asset protection: Shields assets from Medicaid's asset limit and estate recovery programs.

- Preserve family wealth: Protects inheritance for family members and beneficiaries.

- Primary residence protection: Can safeguard your home from being sold to pay for nursing home care.

- Tax advantages: May reduce estate taxes and provide capital gains tax benefits.

- Peace of mind: Ensures access to quality care without depleting life savings.

What Are the Shortcomings of a MAPT?

While highly useful, MAPTS are not entirely without drawbacks. Here are a few disadvantages worth considering.

- Loss of control: Assets transferred become irrevocable and cannot be easily retrieved.

- Five-year waiting period: Must plan well in advance due to the look-back period requirements.

- High setup costs: Initial legal fees can range from $7,000 to $12,000.

- Income implications: Trust income may affect Medicaid eligibility if it exceeds income limits.

- No guarantee: Doesn't automatically guarantee Medicaid approval for all applicants.

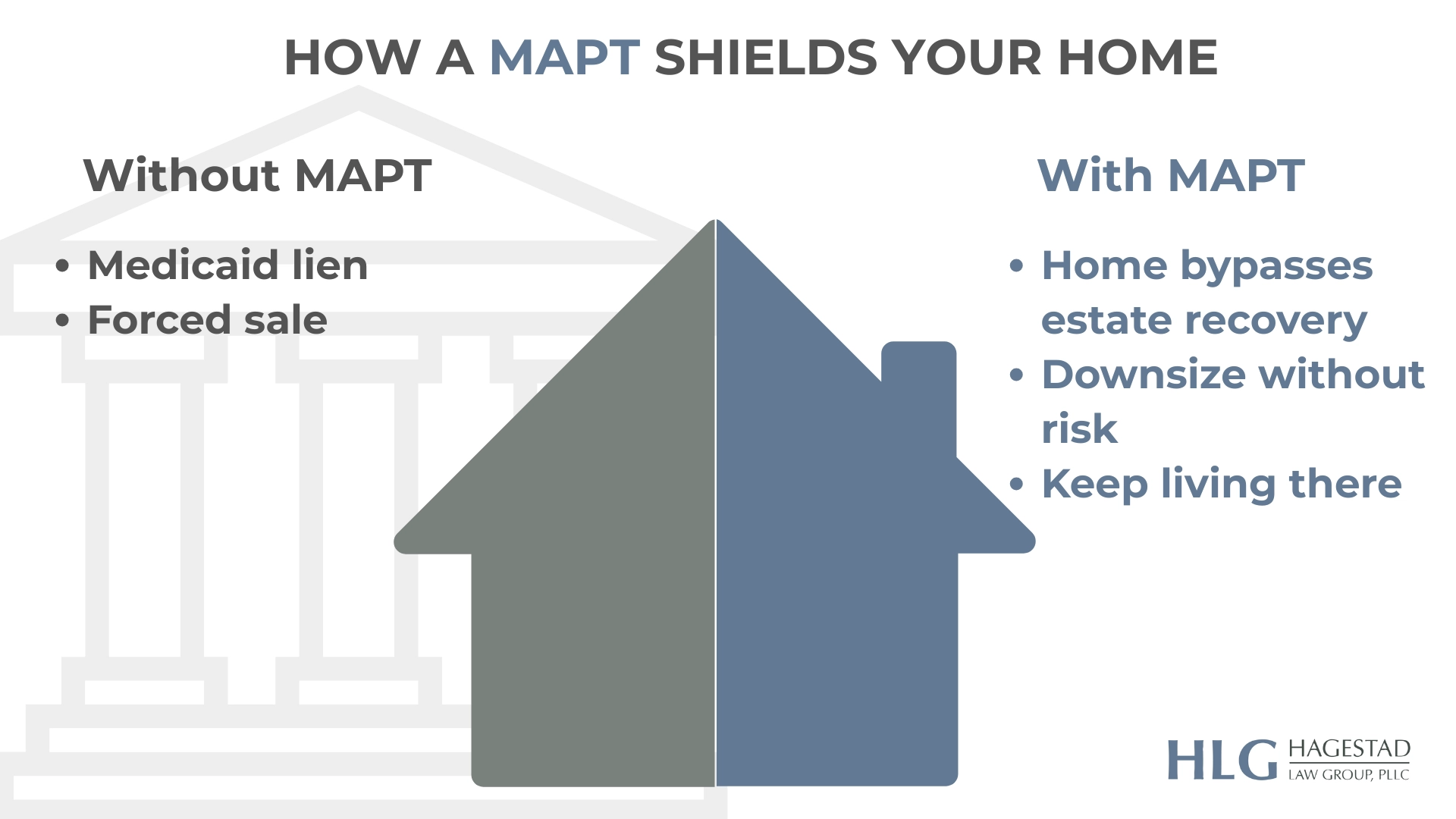

Can You Protect Your Home with a MAPT?

Yes, you can protect your primary residence using a MAPT, even though Medicaid typically exempts your home from countable assets during the application process.

Upon the recipient's passing, state Medicaid agencies commonly seek reimbursement for care expenses by placing liens against the deceased's estate, which may include their family home. By implementing a MAPT as part of a comprehensive planning strategy, homeowners can mitigate this risk.

MAPTs offer a level of flexibility, allowing homeowners to downsize to smaller residences while shielding their new properties from Medicaid. Despite the irrevocable nature of MAPTs, certain provisions within the trust structure enable homeowners to retain control over key aspects, such as trustees or beneficiaries.

What Assets Can Be Placed in a MAPT?

Understanding which assets qualify for MAPT protection helps you make informed decisions about your estate planning strategy. Most personal property and financial assets can be transferred, though some retirement accounts require special handling before placement in the trust.

- Bank accounts and savings accounts

- Investment portfolios and brokerage accounts

- Real estate properties (including primary residence)

- Certificates of deposit (CDs)

- Stocks, bonds, and mutual funds

- Business interests and partnerships, especially when they involve family business protection

- Personal property with significant fair market value

- Life insurance policies with cash value

Important note: Certain assets, such as many retirement plans and IRAs, may need to be liquidated before being transferred to a trust.

In some states, transferring one's primary home into a MAPT may not provide complete protection from Medicaid. Nonetheless, MAPTs allow homeowners to continue residing in their homes while benefiting from asset protection strategies.

While income-producing assets placed in the trust may generate income, the trustmaker must consider Medicaid's income limit to ensure continued eligibility for benefits.

Overall, MAPTs can be a versatile mechanism for protecting assets and satisfying Medicaid eligibility criteria.

How Much Does It Cost to Create a MAPT?

Creating a MAPT typically costs between $7,000 to $12,000, depending on several factors, including your location, the attorney's experience, and the value of assets transferred.

While this initial investment may seem substantial, the long-term savings often outweigh the upfront expense.

Given that the national average cost of nursing home care exceeds $7,900 per month, a MAPT can prove to be an effective strategy for avoiding substantial out-of-pocket expenses for long-term care. The cost varies based on whether the trust is part of a comprehensive estate planning package, your marital status, and the need for crisis planning. Urban areas generally have higher legal fees than rural locations, and more experienced estate planning attorneys command premium rates for their services.

Is an Attorney Needed to Set Up a MAPT?

Setting up a Medicaid Asset Protection Trust requires meticulous attention to detail to guarantee compliance with Medicaid regulations. Since these regulations frequently evolve and vary by state, it's crucial to establish the trust correctly to make transferred assets exempt from Medicaid's asset limits.

Given the complexity and potential consequences of errors, it’s advisable to rely on an attorney well-versed in the laws relating to MAPTs.

An experienced elder law attorney will have the knowledge and foresight to effectively handle state-specific requirements, reducing the risk of inadvertently jeopardizing your Medicaid eligibility. Collaborating with a private Medicaid planner who works in conjunction with legal professionals can help streamline the process while keeping costs manageable. This helps avoid the risks of DIY estate planning, which can lead to invalid or ineffective trusts.

What Are Alternatives to a MAPT?

Beyond MAPTS, several alternative planning strategies exist to reduce countable assets and qualify for Medicaid, including spend-down methods and other asset protection strategies tailored to individual goals.

Spend-Down Strategies involve countable assets by reallocating them to non-countable ones, thereby meeting Medicaid's asset limit (home improvements, prepaid burial expenses, or medical equipment).

Individuals might also consider irrevocable funeral trusts, which allocate funds for funeral and burial expenses to make them exempt from Medicaid eligibility calculations. Another option is Medicaid-compliant annuities, which allow individuals to convert assets into income streams that comply with Medicaid regulations.

Furthermore, various financial planning strategies can help taxpayers decrease their countable income levels and achieve Medicaid eligibility. These alternatives permit individuals to tailor their estate plans to meet established Medicaid requirements.

What Are the Steps in Creating a MAPT? How Do You Avoid Possible Mistakes?

Setting up a Medicaid Asset Protection Trust involves several key steps:

- Consult an experienced attorney: Qualified estate attorneys like those at HagEstad Law Group are essential for navigating the intricate procedures involved in forming a MAPT.

- Conduct a comprehensive assessment of your assets: Doing so will help you determine which assets are eligible for transfer into the MAPT.

- Draft a trust document: Your trust document must contain clear terms and trustee responsibilities, accompanied by an understanding of trustee duties and liabilities.

- Fund the trust: Transfer your assets into the MAPT to complete the setup process; this may require changes in titles or beneficiary designations.

To avoid potential pitfalls when establishing a MAPT, you must take care to avoid certain mistakes. One common error is improper funding, which happens when ineligible assets are transferred into the trust, leading to legal and financial complications.

Failing to seek guidance from reliable legal and financial professionals throughout the process can result in Medicaid officials declaring your MAPT invalid, undermining the intended asset protection objectives.

Protecting Your Financial Future with MAPTs

Medicaid Asset Protection Trusts are indispensable for safeguarding your assets and ensuring that you qualify for Medicaid benefits. By establishing a MAPT, you can shield your assets from the program’s stringent requirements, ensuring smoother access to essential care while preserving your legacy for future generations.

While MAPTs offer numerous benefits, it's important to recognize their potential limitations and seek out alternatives when necessary.

As a law firm serving both Montana and Arizona for years, HageStad Law Group has extensive experience in Medicaid planning and asset protection strategies for clients facing potential long-term care needs. Contact our office today to discuss how a MAPT might fit into your estate plan and protect your family's financial security.

Secure Your Family's Future with Hagestad Law Group

Work with our dedicated estate planning attorneys at HagEstad Law Group to create a comprehensive strategy that protects your assets and guarantees access to the care you might need later in life.